Who should generate an E-way bill?

The following cases wherein a person having GST registration are causing goods movement should generate an E-way bill.

How to Generate E-Way Bill

An E-Way Bill (EWB) is an ‘electronic way’ bill for movement of goods which can be generated on the E-Way Bill Portal. Any supplier or a transporter transporting goods with a value of more than Rs.50,000 (Single Invoice/bill/delivery challan) in a single vehicle should carry a GST e-way bill as per the GST Council regulations. The supplier or the transporter of the goods must register with GST to obtain GST E-Way bill. This bill shall come into effect from 1st April 2018.

After generating the E-Way bill on the portal using required credentials, the portal generates a unique E-Way Bill Number (EBN) and allocates to the registered supplier, recipient, and the transporter. In this article, we look at the steps to generate a e-way bill on the Government website.

The supplier or the transporter can create the E-way bill through the following ways:

Steps to Generate E-Way Bill through Website

E-way bill can be generated on the GST E-Way Portal. To use the portal, you will need a GST registration and transporter registration.

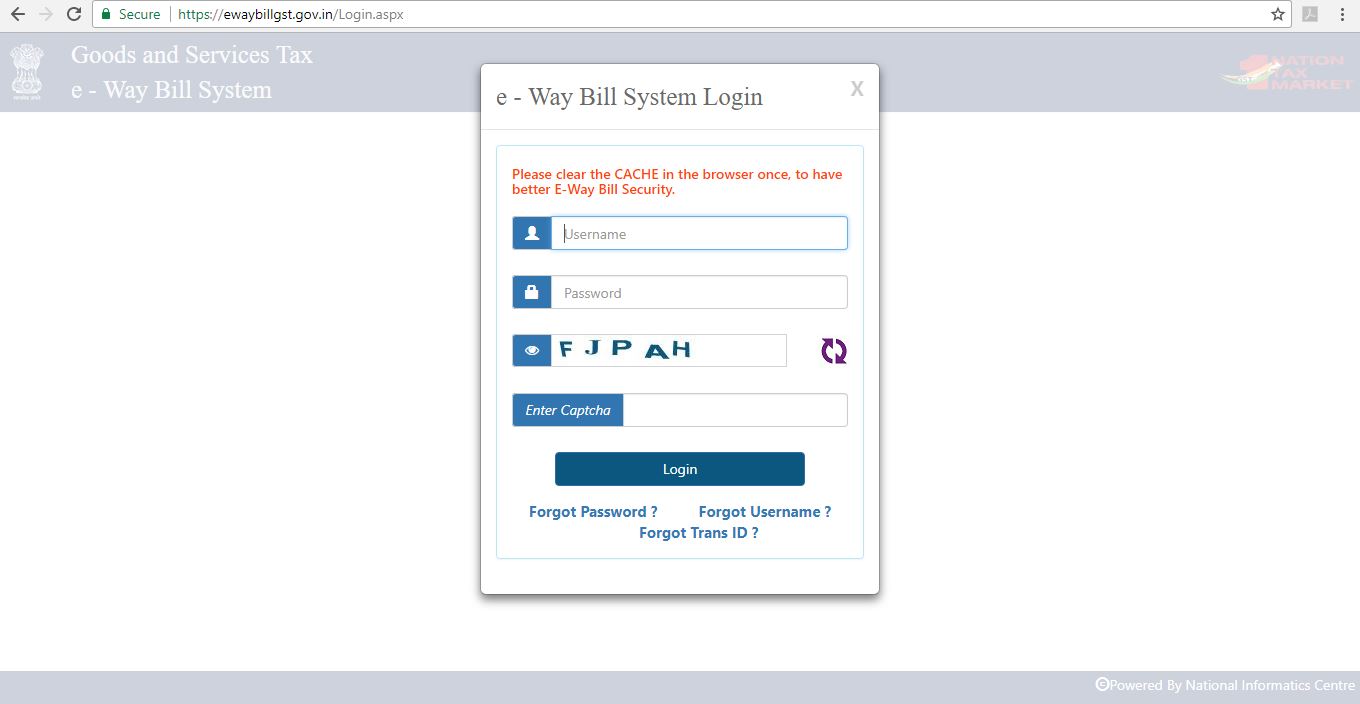

Setp 1: Access the E-Way bill generation portal at https://ewaybill.nic.in/ and enter the login detail to enter the platform.

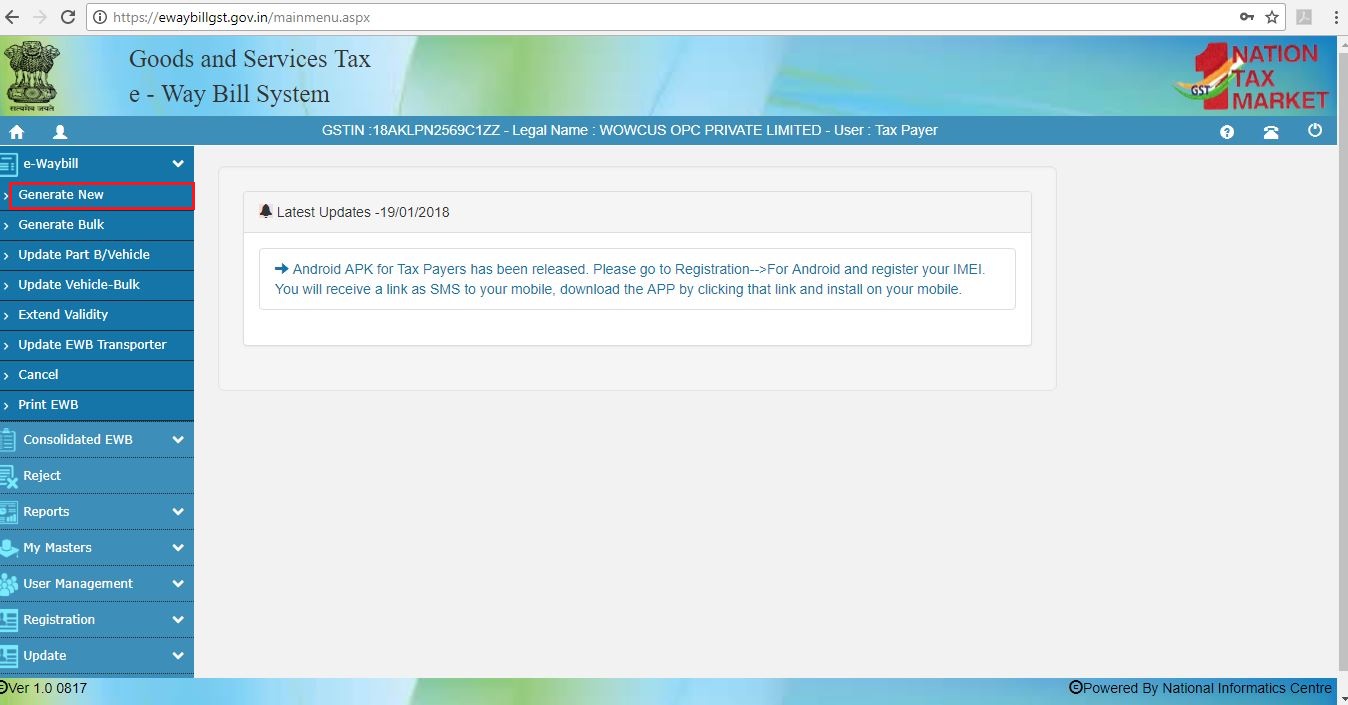

Setp 2: Click on the “Generate New” option from the E-Way bill- Main menu page to create a new E-Way bill.

Generate E-Way Bill

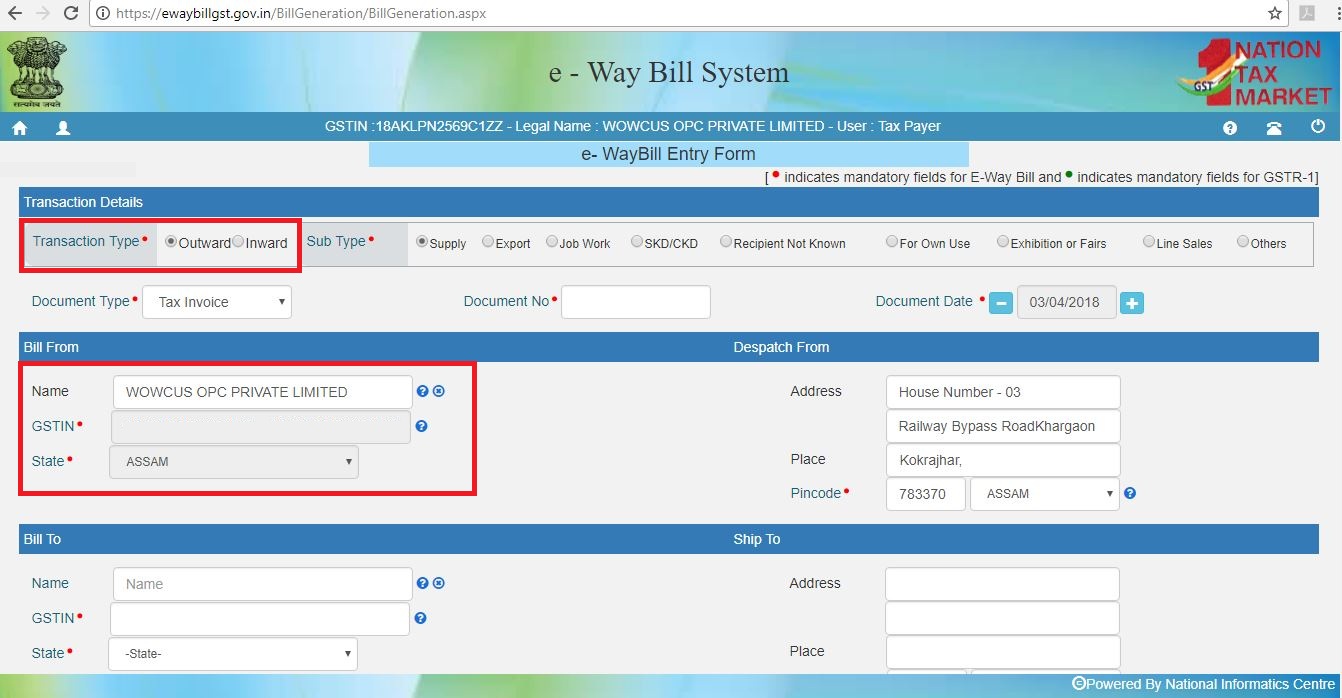

Setp 3: A new EWB bill generation form appears. Fill in the details required similar to creating a GST invoice.

Select outward, if you are the supplier and inward, if you are the recipient. Enter details of the supplier and recipient along with GSTIN, wherever applicable.

When a registered GSTIN is entered in the field provided in the form, other details gets pulled into the empty fields. Before proceeding to the next step kindly check the details.

Enter Goods Description

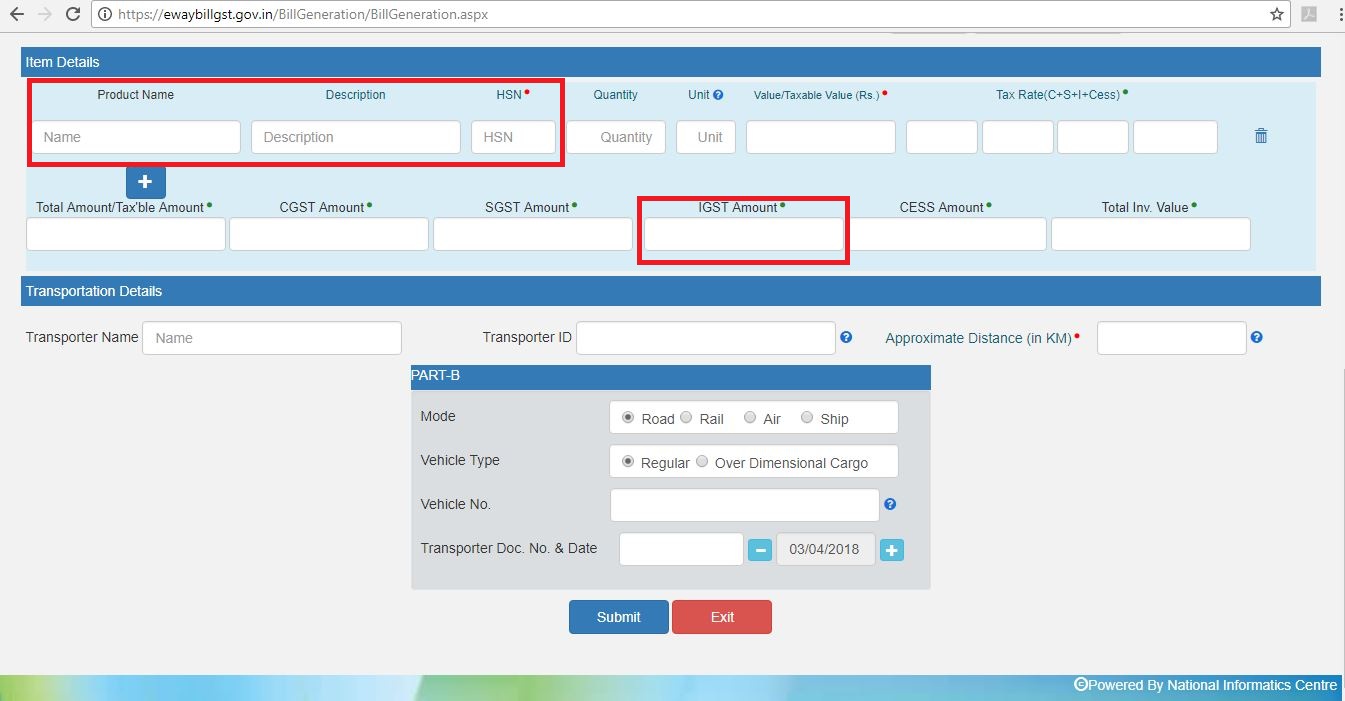

Setp 4: The second half of the page will contain information to be filled as follows:

Setp 5: Generate E-way bill

After filling all the necessary details, click on the “SUBMIT” button to create the EWB. The Portal shall display the E-Way bill containing the E-Way Bill number and the QR Code that contains all the details in the digital format. The printed copy of the bill should be provided to the transporter who will carry it throughout the trip till it is being handed over to the consignee.

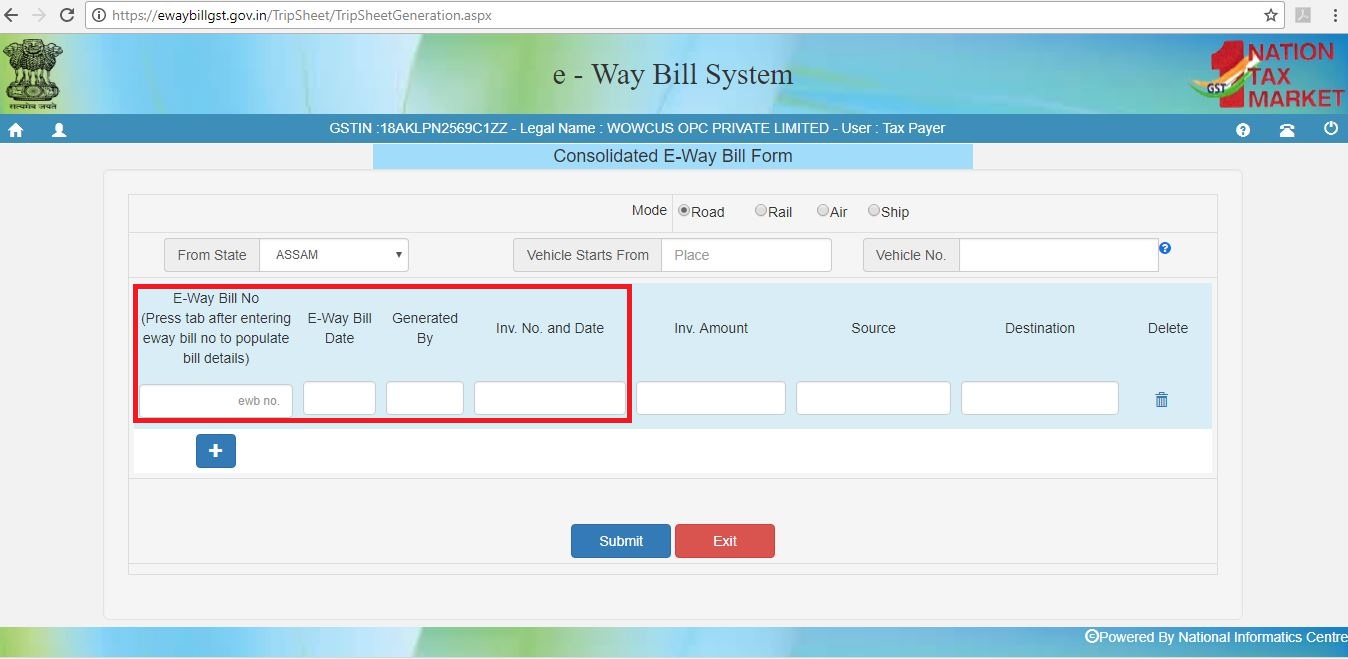

Setp 6: Consolidate E-way Bill Generation

A consolidated EWB can also be created which contains all the details on the transaction and is also easy to create it by providing just the ‘E-Way bill number’ in the required field. Click on “SUBMIT” to generate the consolidated EWB.

An E-Way bill can be updated once it is created. Details on the transporter, consignment, consignor and also the GSTIN of both the parties can be updated in the existing E-Way bill provided the bill is not due on its validity.

The validity of the eWay Bill

What is the minimum distance required for E-way bill?

The significant amendment made effective video notification no. 12/2018- Central tax dated 7th March 2018 changes in the validity period of E-way bill. The new validity period provisions of the E-way bill are tabulated here:

| Type of Conveyance | Distance | E-way bill |

|---|---|---|

| Other than Over dimensional cargo | Less than 100 km | 1 day |

| For every additional 100 km and thereof | Additional 1 day | |

| For Over dimensional cargo | Up to 20 km | 1 day |

| For every additional 20 km and thereof | Additional 1 day |

The relevant date on which the E-way bill has been generated and the period of validity would be counted from the time at which the E-way bill has been generated, and each day would be counted as the period expiring at midnight of the day immediately following the date of generation of the E-way bill.

‘Over Dimensional Cargo’ is a cargo carried as a single indivisible unit and which exceeds the dimensional limits prescribed in rule 93 of the Central Motor Vehicle Rules,1989, made under the Motor Vehicles Act,1988 (59 of 1988).

SMS E-way Bill Operation

SMS e-way bill generation is ideal for entities with limited transactions, as it would be prudent to use other methods in case of higher volume.

SMS e-way bill generation facility can also be used by taxpayers in case of emergencies such as during the night or while involved in travelling in a vehicle.

Enabling SMS E-Way Bill Facility

Before starting to transact, the taxpayer must first register his/her mobile number on the GST e-way bill portal. The system only enables and responds to mobile number registered on the portal for a particular GSTIN.

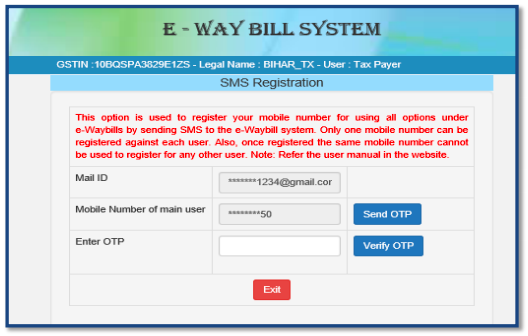

Once user selects option ‘for SMS’ under main option ‘Registration’, following screen is displayed.

The user must enter the mobile number and complete the OTP to register the mobile number.

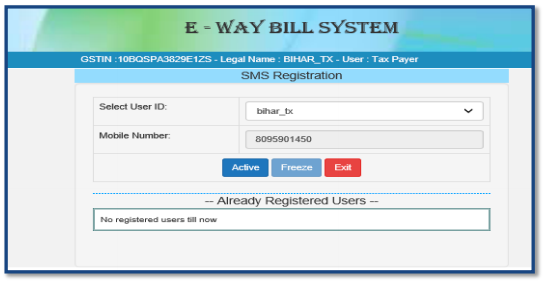

In the next screen the mobile number registered with the GSTIN is displayed. The user can use this screen for delinking or changing the mobile number, if required.

Step 1: Access to Portal

The taxpayer or the transporter must open the e-way bill portal and log in using his/her credentials.

Step 1: Register Mobile Number

Enable the SMS e-way bill facility by following the below shown above. Once validation is complete and the mobile number is registered, you are ready to generate e-way bill using SMS.